Undersea Networked Systems Market to Reach US$13.36bn by 2036

4 June 2026.

Visiongain’s in-depth report examines the global Undersea Networked Systems Market Report 2026-2036, providing detailed forecasts and strategic analysis across defence, commercial, and public safety, technology trends, trade impacts, and leading companies.

Growing investments in underwater communications, AI-enabled sensor networks, autonomous maritime systems, and critical infrastructure protection are accelerating the evolution of the world’s underwater defence ecosystem. The underwater domain is entering a new era of connectivity.

As governments and defence organisations seek to improve maritime awareness, strengthen critical infrastructure protection, and support future naval operations, investment in Undersea Networked Systems is increasing rapidly. The convergence of underwater communications technologies, distributed sensor networks, artificial intelligence, and autonomous maritime platforms is creating a new generation of connected underwater ecosystems capable of delivering persistent situational awareness across strategic maritime regions.

According to Visiongain’s latest market analysis, the global Undersea Networked Systems Market is projected to grow from US$6.47 billion in 2026 to US$13.36 billion by 2036, representing a compound annual growth rate (CAGR) of 7.5% during the forecast period.

The market is benefiting from rising geopolitical competition, growing concerns regarding undersea infrastructure security, and increasing adoption of network-centric operational concepts across naval forces worldwide.

As maritime operations become increasingly data-driven and interconnected, Undersea Networked Systems are emerging as one of the most important technologies shaping the future of maritime defence.

Download Free Sample Report (incl. forecasts, market data, and methodology)

Requirement for Real-Time Sensor-to-Shooter Connectivity and Multi-Domain Data Fusion

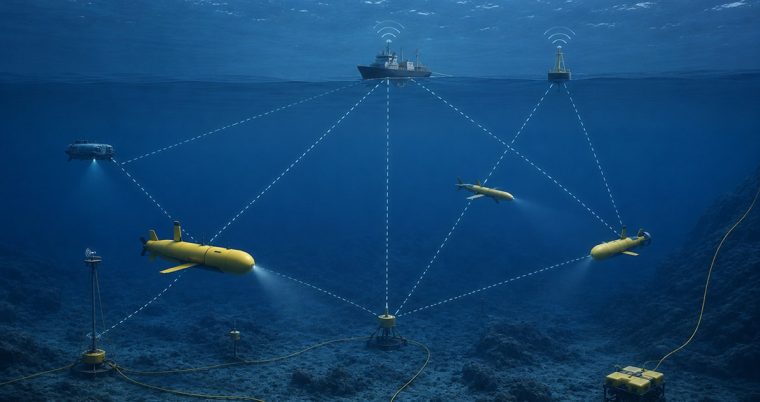

The modernisation of naval tracking tactics has exposed the severe operational risks of isolated sub-surface platforms. Traditional models, where an uncrewed vehicle or deep seafloor array had to wait to be physically recovered or surface to transmit data, are no longer viable in high-threat environments. Global naval commands are aggressively funding Undersea Networked Systems to act as the primary structural backbone linking deep-ocean sensors directly with surface flagships, aerial networks, and space-based nodes. This capability allows defence forces to build a continuous, real-time tactical picture, dramatically accelerating the speed of sub-surface target identification and response times.

Hardening and Interconnecting Sub-Surface Surveillance Choke Lines

The escalating need to secure vital maritime transit lanes and littoral zones against next-generation stealth submarine deployments is straining legacy detached sonar nodes. Navies are responding by installing large-scale, interconnected subsea data routing grids around strategic narrow channels and littoral border boundaries. These systems combine multiple bottom-mounted hydrophone lines, autonomous vehicle docks, and cross-domain gateway acoustic links into a unified, network-centric framework. This interconnected architecture ensures that if a single localized array is disrupted or spoofed by gray-zone interference, the surrounding network nodes automatically re-route telemetry data streams to guarantee continuous monitoring coverage.

Technology and Innovation

Hybrid Acoustic-Optical Modems and Quantum Underwater Encryption Protocols

The defining technological barrier in underwater network development has always been the physics of sub-surface data transmission. To overcome acoustic lag, signal distortion, and low bandwidth over long distances, next-generation systems integrate hybrid communication architectures. These modems automatically switch between long-range acoustic sound waves for baseline tracking data and short-range, ultra-high-bandwidth blue-green laser optical links for rapid data dumps (such as high-definition sonar map transmissions). Furthermore, to prevent adversary interception or jamming of these critical data streams, systems are integrating quantum-cryptographic software interfaces directly into the edge routing modules, securing subsea networks from data interception directly on the ocean floor.

Trade and Supply Chain Considerations

Impact of U.S. Trade Tariffs on the Global Undersea Networked Systems Market

The global industrial base for advanced sub-surface data routing is experiencing significant friction due to strict U.S. trade tariffs and expanded protectionist procurement policies. The imposition of broad tariff frameworks and strict Buy American Act provisions has specifically targeted foreign sourcing of specialised optoelectronic components, advanced deepwater transceivers, and specialised low-loss glass fibre matrices required for military-grade undersea data lines. These trade barriers have injected considerable component cost volatility for major Western defence primes, generating near-term delivery backlogs and extending deployment timelines across multi-year planning horizons.

Concurrently, these trade penalties are forcing a structural division within the allied industrial supply chain. To eliminate dependency risks on foreign manufacturing facilities vulnerable to geopolitical export embargoes or cyber interference, prime defence contractors are rapidly reshaping their manufacturing footprints.

Sovereign acquisition mandates increasingly demand total insulation of the design and assembly base, requiring 100% native software cleanroom coding, specialized acoustic crystal casting, and complete cable assembly inside domestic borders. While these tariffs accelerate localized capital investments within allied nations, they create an intermediate capacity bottleneck, restricting the delivery velocity of tier-2 component manufacturers that rely on non-insulated international logistics loops.

Standardised Universal Underwater Interface Protocols (Open-Architecture Modems)

The legacy reliance on closed, proprietary communications software built by individual defence contractors represents an expansive commercial growth opportunity for agile systems integrators. The market is aggressively pursuing open-architecture undersea communication modems that utilize standardized universal protocols (such as JANUS). This enablement allows disparate subsea platforms, such as a surface drone built by one contractor, an autonomous sub built by another, and a fixed seabed array built by a third—to seamlessly interoperate and share telemetry data on a single network. By breaking open proprietary vendor lock-ins, this standardization compresses naval software integration cycles and lowers procurement cost barriers by up to 65%.

Persistent Subsea Acoustic Telemetry Gateways and Inductive Charging Hubs

The operational requirement to maintain deepwater autonomous networks without deploying expensive surface monitoring ships has unlocked an expansive market opportunity for fixed seafloor networking hubs. Systems integrators are developing permanent, bottom-mounted node frameworks that combine long-life inductive power charging pads with high-bandwidth acoustic telemetry routing gateway switches. These hubs allow passing uncrewed vehicles to dock, recharge their onboard batteries, and automatically dump collected target reconnaissance data streams into a secure subsea network line. This structural arrangement optimizes capital expenditure allocations across allied markets by allowing a small, low-cost network grid to monitor vast underwater corridors completely invisibly.

Competitive Landscape

The major players operating in the undersea networked systems market are Anduril Industries, ASELSAN, Atlas Elektronik, BAE Systems Plc, Curtiss-Wright, DSIT Solutions, Elbit Systems, Exail Technologies, FINCANTIERI S.p.A., General Dynamics, Hanwha Group, Huntington Ingalls Industries, Israel Aerospace Industries, Kraken Robotics, Kongsberg Gruppen, L3Harris Technologies, Leonardo S.p.A., Lockheed Martin, Naval Group, Oceaneering International, Inc., RTX Corporation, Saab AB, Teledyne Technologies, Thales Group, ThyssenKrupp Marine Systems (TKMS). These major players in this market have adopted various strategies, including M&A, collaborations, R&D investments, regional expansion, partnerships, and new product launches.

Recent Developments

- June 2, 2026: Tech giant Google and Australian telecom leader Telstra finalized a major reciprocal infrastructure exchange agreement designed to handle explosive AI and cloud data traffic. Under the contract, Google secures inter-city dark fiber capacity on Telstra’s newly deployed 8,000 km terrestrial Aura Network. In return, Telstra gains direct fiber-pair access to Google’s high-capacity Tabua, Proa, and Bulikula subsea cable systems. This creates resilient, highly secure routing paths linking Australia, Japan, the US, and the Pacific Islands.

- June 2, 2026: Infrastructure developers SUBCO and Firmus announced a landmark agreement to construct the Bernacchi-1 submarine fiber-optic cable connecting Tasmania to mainland Australia. Underwritten by private-sector funding from Firmus, the system will branch into SUBCO’s newly built SMAP cable system. Bernacchi-1 marks the first new subsea data pathway across the Bass Strait in over 20 years, delivering over 60 terabits per second of additional undersea network capacity to support regional AI computing infrastructure.

- May 17, 2026: Alcatel Submarine Networks (ASN) successfully executed a long-distance, dual-use breakthrough using its SMART Climate Change (CC) solution. Operating directly from its corporate headquarters in Les Ulis, France, the company successfully utilized active underwater communication fiber arrays to detect a major earthquake in Japan over 9,000 miles away. This milestone demonstrates how commercial undersea data networks can serve a secondary purpose as live, planetary-scale fixed seabed acoustic and seismic monitoring systems.

- May 17, 2026: Private equity giant Cerberus Capital Management successfully closed a $2.3 billion single-asset continuation vehicle for SubCom (Subsea Communications). Representing one of the largest secondary transactions in the history of the subsea cable market, the financial restructuring significantly extends Cerberus’s ownership of America’s premier submarine network manufacturer. The capital infusion will directly fund SubCom’s expanding global order book for hyperscale and defense undersea routing hardware.

- April 22, 2026: GCI Holdings LLC (a subsidiary of GCI Liberty, Inc.) concluded a definitive corporate agreement to acquire 100% equity in Quintillion from Grain Management LLC. The transaction consolidates critical Arctic communications infrastructure by merging Quintillion’s 1,800+ miles of active subsea and terrestrial fiber cables with GCI’s statewide operating network. The acquisition enables highly secure routing expansions across contested northern maritime zones.

Download Free Sample Report (incl. forecasts, market data, and methodology):

About Visiongain

Established in 1998, Visiongain is an independent publisher of analyst-led market intelligence, delivering data-driven research, forecasts, and strategic insight across global industries and emerging markets. Visiongain supports evidence-based decision-making for investment, procurement, and long-term strategic planning.

Media Contact

press@visiongain.com

+44 (0)20 7336 6100

www.visiongain.com